9/2022

By Walton Cobb, CFP®

Fall is in the air, and children are back in school for a new year. A sense of optimism usually follows each change of season. However, for investors in 2022, each season has brought the same doom and gloom. The S&P 500 is down over 23% year to date, the Nasdaq Composite is down over 31%, the Russell 2000 (small cap index) is down over 23%, and broad based foreign stocks are down over 27%1. What is most troubling of all? The impact that rising interest rates have had on the bond market. Year-to-date, the 10 Year Treasury is on pace for its worst return on record 2. Wait, we invest in the bond market to reduce risk and be “safe”, right? A new season indeed!

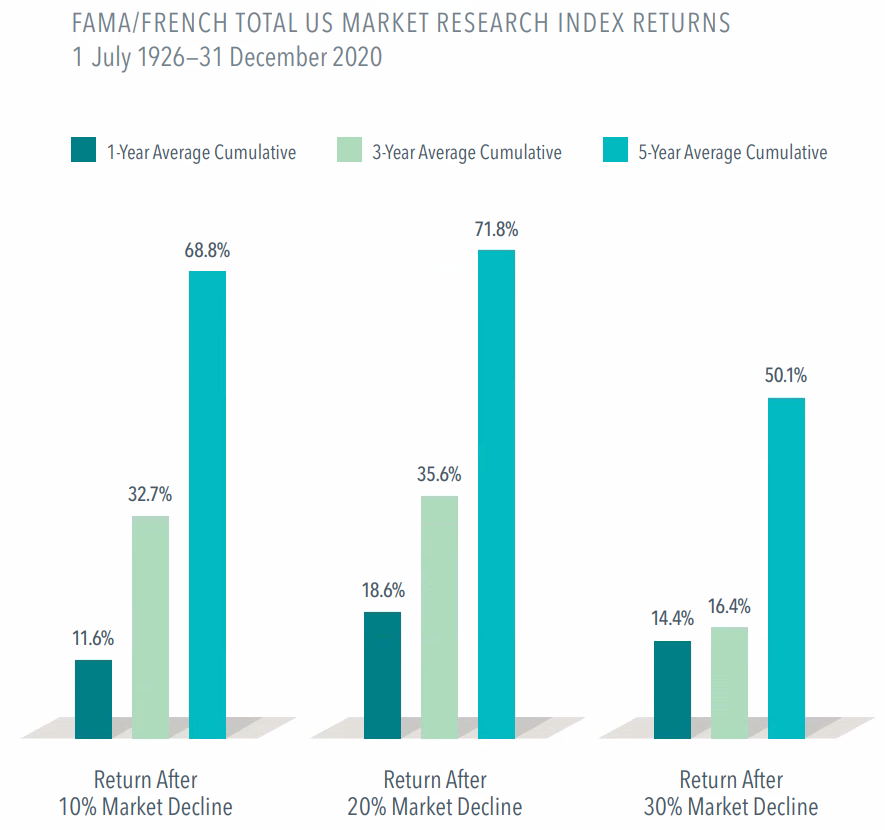

As the sun rose yesterday morning revealing the horrid images of Hurricane Ian’s destruction, we are reminded of how little we control in the short term. Clearly human life is more valuable than any investment portfolio, but there is a parallel here. One does not move to the Florida coast without accepting the risk of Mother Nature’s tropical rage and few permanently flee after a storm recedes. Why? Simply put, there are many more sunny days in Florida than not. Just as every hurricane ends, bear markets do as well. Although every economic recession and bear market is different in how it begins, the results are generally the same. Markets decline, sometimes precipitously, and then the cycle begins anew, eventually to reach new heights. In 2008, the S&P 500 fell by 37%, but bounced back 26.46% and 15.06% in 2009 and 2010, respectively 3. In fact since 1996 the S&P 500 has only had 5 down years, which means during that time period there were many more sunny days than not 3.

At Cahaba, our job is to coach our clients through the good times and the bad by helping you minimize the role emotion plays when making financial decisions. The data overwhelmingly shows that the only way to withstand a bear market is to “control the controllables”. These “controllables” include tax loss harvesting, diversification, rebalancing, cash flow projection revisions, media consumption and most importantly your reactions. What can we not control in the short term? GDP, market performance, inflation, the Federal Reserve, corporate earnings, which party is in control of Congress… you get the idea.

One of the most difficult behaviors that we battle is our own consumption of mass media. Should you find yourself watching too much CNBC or reading too many negative voices on social media, turn the television off and put down the phone. These voices are intentionally appealing only to your fears. No matter how smart the media pundits seem, no one can foresee the future. The timing of economic recessions and market crashes are rarely ever accurately predicted. As we witness daily, when it comes to investment managers there are very few good stories, but thousands of storytellers. Anyone can be right over a 3 year period and completely wrong over the next 3.

As a team, we are committed to a data driven approach to portfolio management. We will not pretend to know what the near term will bring us. However what we do know is that the water will recede and most importantly, we know you. Throughout the financial planning process, we learn your investment objectives, risk tolerance, time horizon, current/future tax brackets, future expected expenses, insurance needs, and what to expect for your family long after you are gone. With the markets down, it is also a great time to “stress test” your long term cash flow projection for any potential long term hiccups.

Human nature tells us to take action and stop the bleeding. During many other crisis situations, that may be an appropriate response. However, when considering long term investment success, we must be in the markets on the very first day of its return to glory, as it will never be available to you again. Since we don’t know exactly when that day will come, we have to weather the storm through its worst days. As a firm, we have witnessed multiple economic recessions coupled with bear markets. In all cases, the thing to do was to remain invested. The odds are overwhelmingly in our favor that history will repeat itself again. In the meantime, we have to “control the controllables”. We remain confident that the changes of season will soon bring more optimism, and we look forward to many more sunny days ahead.

Walton Cobb, CFP®, is a financial advisor in the Birmingham office of Cahaba Wealth Management, www.cahabawealth.com.

1 Source: Stocks. (n.d.). Retrieved September 30, 2022, from https://ycharts.com/stocks

2 Source: Bahceli, Y. (2022, June 30). Bonds in line for worst year in decades. Reuters. Retrieved September 30, 2022, from https://www.reuters.com/markets/rates-bonds/brutal-first-half-puts-bonds-line-worst-year-decades-2022-06-30/

3 Source: S&P 500 total returns by year since 1926. (n.d.). Retrieved September 30, 2022, from https://www.slickcharts.com/sp500/returns

Cahaba Wealth Management is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by the SEC nor does it indicate that the adviser has attained a particular level of skill or ability. Cahaba Wealth Management is not engaged in the practice of law or accounting. Always consult an attorney or tax professional regarding your specific legal or tax situation. Content should not be construed as personalized investment advice. The opinions in this materials are for general information, and not intended to provide specific investment advice or recommendations for an individual. Content should not be regarded as a complete analysis of the subjects discussed. To determine which investment(s) may be appropriate for you, consult your financial advisor.